Credit Union vs. Bank Differences

Member-owner or just a customer?

While both credit unions and banks are institutions designed to help with your financial needs, the two actually have a few very notable differences.

What is a bank?

Banks are for-profits owned by stockholders or investors. You might be asking yourself what this means if you’re a bank customer. It’s simple: any profits made by a bank are used to pay out dividends to stockholders, which means that you don’t directly benefit from being a bank customer unless you own shares of the company.

What is a credit union?

Credit unions are run in a way that benefits members directly. It all starts with the fact that credit unions are owned by stakeholders, aka, you! In other words, banks are public organizations, while credit unions are not-for-profit.

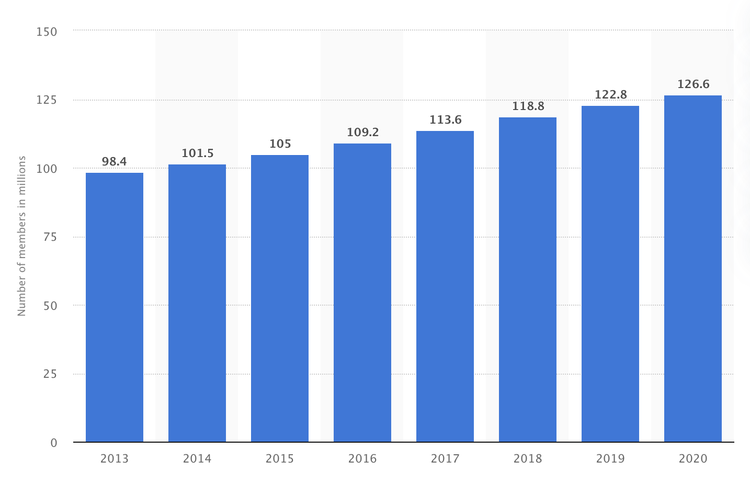

According to the National Credit Union Administration, there were more than 5,000 credit unions with over 120 million members as of December 2020.

The credit union motto is “People Helping People,” and it’s no wonder because credit union members quite literally borrow money from one another. Think of the way credit unions operate as a closed-loop: members work with other members to save money so that other members can borrow that same money.

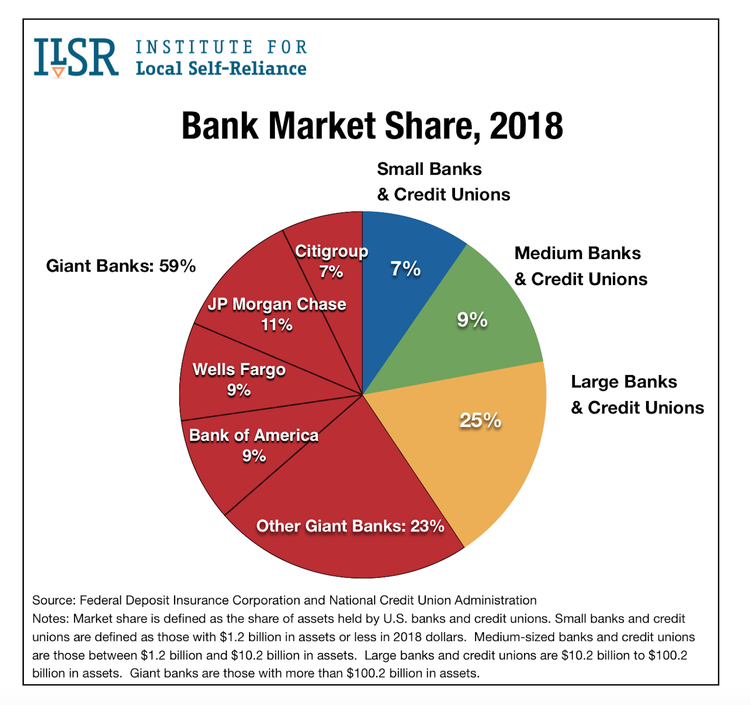

From the Institute for Local Self-Reliance. Source: Federal Deposit Insurance Corporation and National Credit Union Administration Notes: Market share is defined as the share of assets held by U.S. banks and credit unions. Small banks and credit unions are defined as those with $1.2 billion in assets or less in 2018 dollars. Medium-sized banks and credit unions are those between $1.2 billion and $10.2 billion in assets. Large banks and credit unions are $10.2 billion to $100.2 billion in assets. Giant banks are those with more than $100.2 billion in assets.

Credit union field of membership

Most credit unions require that you live, work, worship, or go to school in a certain area of the credit union, while others require that you also work a certain type of job in order to qualify for membership. Meanwhile, anybody can become a bank customer.

Number of members of credit unions in the United States from 2013 to 2020 (in millions, shown in the graphic below):

| Year | Number of Members (in millions) |

|---|---|

| 2013 | 98.4 |

| 2014 | 101.5 |

| 2015 | 105 |

| 2016 | 109.2 |

| 2017 | 113.6 |

| 2018 | 118.8 |

| 2019 | 122.8 |

| 2020 | 126.6 |

Source: Statista.com

Bank stakeholders versus credit union ownership

The private ownership credit unions offer members is a big reason why savings accounts are known as “share accounts” at these not-for-profits. When members take out loans at credit unions, they borrow money from other members. This also explains why members of credit unions are called “members.”

If you have an account at a bank, you’re known as a customer, not a member, because the money borrowed from loans does not come from others that are part of the organization. Banks are therefore funded by investors, just like other public businesses.

As a small business owner, #bankofamerica is exactly why I do business with a local credit union.

— Kaz Weida (@kazweida) April 3, 2020

Corporate banks don’t care about you or your community.

Credit union loan and savings rates

Credit unions are traditionally known for having a community-feel and friendly service. They are also known for offering lower rates on loans, making them a great option if you are considering buying a new car or purchasing your first home, or even if you want to refinance. Expect lower and fewer fees when you join a credit union.

While banks are known for their convenience, like having more available ATMs and branches nationwide, you’re likely to pay more interest on loans you take from a bank.

Credit unions may be limited to the region, county, or city they’re in. However, credit unions every day are implementing co-op financial services (ATMs you can easily access with no fees even if you are not a member of that specific credit union), updated mobile apps, and more. The co-op shared branch network of certain credit unions has 5,600 branches and 54,000 surcharge-free ATMs that can be used, whether you’re a member of that credit union or not.

Due to being for-profit financial institutions, banks find it hard to compete with credit unions when it comes to lower interest rates and fees. You may end up paying more in bank fees for errors, such as bounced checks or overdrafts. The same goes for interest rates on loans and savings accounts.

According to the NCUA, which regularly compares the rates for credit unions versus banks, credit unions produced higher interest rates on Certificates of Deposit (CDs), money market, and savings accounts while also posting lower interest rates on home and auto loans during the first quarter of 2020.

Become a member at AFL-CIO Employees Federal Credit Union!

AFL-CIO Employees Federal Credit Union is a community-based credit union that is run democratically. We offer checking and savings accounts, real estate, auto loans, as well as personal loans to our members. Visit our 'Join the Credit Union’ page to join the best credit union in Washington, D.C.

Consider what you want your financial institution to do for you, and remember to trust the organization that you choose!

Come visit our credit union

IN-PERSON OR ONLINE

Visit the AFL-CIO EFCU home page

MAIN BRANCH AND MAILING ADDRESS

555 New Jersey Avenue, NW, Suite 100

Washington DC, 20001

Hours of operation

Monday - Friday: 8:30am to 4:00pm

PHONE NUMBERS

Phone: (301) 683-2800

Fax: (202) 393-3137

24 HOUR TELEPHONE BANKING (AMIE)

Phone: (202) 637-8855